Fintech founders building payments infrastructure on platforms like Stripe and Adyen have more power than ever before. With the right stack, you can launch globally from day one, but the new challenge is knowing how to combine flexibility, scale, and control as your company grows. Both Stripe and Adyen offer world-class infrastructure and each can take you far, but the smartest founders go further, layering orchestration, compliance, and multi-provider resilience into their payment architecture.

In this article, we’ll walk through a few practical steps drawn from real experience: how to choose the right mix of PSPs instead of relying on one, add a payment orchestration layer for resilience and higher approvals, design for compliance and SCA from day one, and leverage leading platform features without getting locked in. But first, let’s take a closer look at what makes Stripe, Adyen, and the next generation of fintech infrastructure so powerful.

Stripe: Built for Builders

Stripe’s superpower is flexibility. Its developer-first APIs make it easy for fintech teams to spin up new features fast, whether that’s issuing virtual cards, running multi-party payouts, or embedding lending and treasury products directly into your platform.

Think of Stripe as a financial toolkit: you pick the modules you need (Connect, Issuing, Capital, Treasury) and plug them into your workflow. Stripe enables the instant creation of cards, multiparty payouts, embedded lending, and deep integration of identity and data connections, letting startups monetize platforms and orchestrate complex payment flows with minimal technical friction. Stripe’s focus on simplifying developer experiences and offering reliable documentation makes the stack ideal for agile fintech teams looking to experiment and iterate quickly.

Adyen: Unified End-to-End Enterprise Infrastructure

Adyen takes a different approach — it’s a unified, enterprise-grade platform that connects directly to global card networks and local payment rails, eliminating third-party dependencies. If you’re building for multiple markets or handling both online and in-person transactions, Adyen’s “single platform” model is a huge advantage. It supports unified commerce, provides deep analytics, and offers direct banking licenses to simplify regulatory hurdles. You get real-time insights, AI-powered conversion tools, and the infrastructure to go global without losing sleep over complexity.

| Feature / Aspect | Stripe | Adyen |

| Core Concept | Modular, developer-first toolkit | Unified, enterprise-grade platform |

| Best For | Agile fintech startups, rapid experimentation | Large merchants, global scale |

| Architecture | Plug-and-play API modules | Single platform connecting directly to card networks and local rails |

| Strength | Flexibility, speed, developer experience | Global reach, operational control, analytics |

| Pricing Model | Flat-rate, predictable | Interchange++ (cost-efficient at scale) |

Vertical SaaS and Embedded Finance Strategies

A new generation of players — like Embed — are taking the “payments-as-a-service” idea further. They focus on vertical SaaS: tailored financial infrastructure for specific industries.

These platforms let you do things like onboard merchants in phases, manage multiple ledgers, or embed industry-specific financial products. It’s about customizing your payments layer instead of accepting generic templates. For founders, that means you can move faster in niche markets, create new revenue streams, and integrate features like global payouts, open banking payments, or instant onboarding without starting from scratch.

Taken together, Stripe, Adyen, and emerging embedded-finance platforms form the backbone of modern fintech infrastructure. But as your transaction volume, markets, and regulatory exposure grow, relying on a single provider starts to limit flexibility and performance.

That’s where strategy matters — not only choosing which PSP to start with, but how to design the right mix from the beginning. Here’s what to do — step by step.

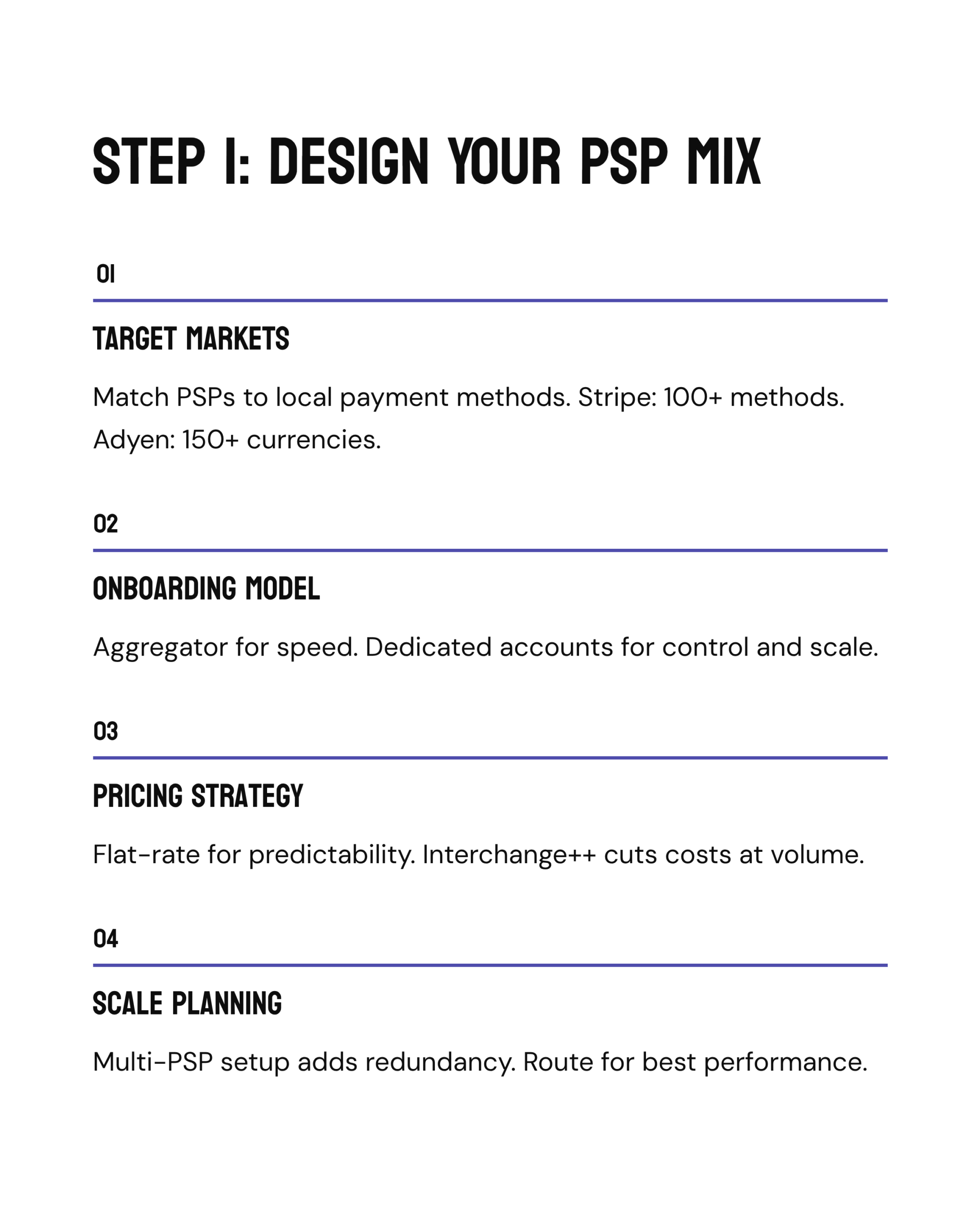

Step 1: Pick the Right PSP Mix Instead of “One Provider”

We get it: when you’re moving fast, picking Stripe and calling it a day feels like the smart move. But that shortcut can cause you a headache in the future.

Once your product crosses borders or starts serving new customer segments, a single PSP (payment service provider) begins to limit your flexibility, margins, and reach. The smarter play is to design a mix of PSPs tuned to your target markets, onboarding model, and pricing realities.

It’s a little more work upfront, but it gives your startup resilience and control, especially as you expand globally or handle diverse payment types.

Target Markets & Local Payment Methods

No single PSP dominates everywhere. Partnering with multiple providers lets you offer the payment methods your users already trust in each region — a direct driver of conversion and customer satisfaction.

- Stripe gives access to 100+ local methods out of the box.

- Adyen goes deeper, connecting directly to card networks and supporting 150+ currencies and regional options like iDEAL (Netherlands), Boleto (Brazil), and SEPA (Europe).

When you test multiple PSPs side by side, you’ll quickly see where acceptance rates differ. One provider might outperform in cross-border transactions, another in recurring payments. Treat this as ongoing experimentation and measure what works (not just what integrates fastest).

Onboarding Model: Aggregator vs. Dedicated Merchant Account

PSPs follow two main models for onboarding merchants:

- Aggregator model (e.g., Stripe):

You’re onboarded under Stripe’s master merchant account. It’s fast, simple, and low-friction, which is perfect for early-stage startups. The trade-off? Less control over underwriting, risk management, and sometimes slower issue resolution. - Dedicated merchant account (e.g., Adyen):

Your business gets its own merchant ID and direct acquirer relationship. That means more flexibility, higher transaction limits, and deeper access to payment schemes — but with more documentation and longer approval cycles.

A multi-PSP setup lets you combine the best of both: rapid onboarding for MVPs or new markets, and dedicated accounts where you need custom flows or regulatory precision.

Pricing Model: Flat Rate vs. Interchange++

The next big decision is how you pay for transactions.

- Stripe uses a flat-rate model — predictable, transparent, and great for founders focused on cash-flow clarity.

- Adyen leans toward interchange++, where fees reflect actual network costs plus a small markup. It’s more complex, but at scale, it can dramatically cut costs, especially for high-volume or cross-border transactions.

Running multiple PSPs gives you pricing agility. Route expensive international or premium card payments to the provider that handles them most efficiently. Over time, that small optimization can compound into significant savings.

Scale and Total Payment Volume (TPV)

Your TPV (total payment volume) should shape your PSP architecture.

- For fast-moving startups, Stripe’s developer-centric APIs and modular design make it easy to iterate and scale quickly.

- For enterprises or unified commerce models, Adyen’s direct network connections and omnichannel coverage (web, mobile, POS) are built for high resilience and negotiation leverage at large volumes.

Using multiple PSPs also adds redundancy. If one goes down or slows settlements, you can reroute transactions instantly — an advantage when uptime equals revenue.

Strategic Advice for Fintech Founders

- Maximize geographic reach using a PSP mix aligned to each market’s payment landscape.

- Test and benchmark onboarding models to balance speed, control, and regulatory fit.

- Use orchestration platforms to route payments for best acceptance and lowest cost, minimizing operational complexity.

- Regularly assess TPV and pricing models to recalibrate PSP allocation for efficiency and scale.

Stripe remains the flexible, developer-oriented choice for startups and rapid experimentation, while Adyen is preferred for unified commerce, dedicated merchant accounts, and interchange pricing scenarios in high-volume or complex enterprises. For fintech founders, the optimal payments infrastructure is rarely built around a single PSP; choosing the right mix maximizes market reach, resilience, and operational efficiency.

Step 2: Add a Payment Orchestration Layer for Resilience and Growth

At some point, every fast-scaling fintech hits the same wall: payments become complex. Different markets, card types, currencies, and providers. Each adds friction, failure points, and hidden costs.

A payment orchestration layer fixes that by acting as the “brain” of your payments infrastructure. Instead of relying on a single PSP, you integrate once with the orchestration platform, which then connects to multiple gateways and local payment methods, automatically rerouting failed transactions (“cascading retries”) and optimizing for cost, speed, or region.

Smart Routing and Cascading Retries

A payment orchestration platform uses smart routing rules to select the best-performing PSP for each transaction based on factors like card type, location, transaction value, or historical gateway reliability. If a payment attempt fails (due to downtime, issuer issues, or PSP-specific logic), the orchestration layer can instantly reroute the transaction to an alternative provider, dramatically reducing false declines and boosting approval rates by as much as 10–15%. This “cascading” process is automated, ensuring that no customer is lost to preventable errors or weak international payment rails.

Adding Local Payment Methods with Ease

As a business expands into new regions, supporting popular local payment methods (like iDEAL in the Netherlands or Boleto in Brazil) becomes critical for maximizing conversion. A payment orchestration layer centralizes these integrations, so new payment options can be quickly added via the orchestrator’s pre-connected network — no need to negotiate, code, or test every integration from scratch. That flexibility lets fintechs move fast, launch new markets with confidence, and keep the checkout experience consistent worldwide.

Why Founders Love It: Four Extra Wins

- No more downtime domino effect. If one PSP fails, payments automatically switch to another — ensuring “always-on” processing and protecting your revenue stream.

- Orchestration layers can automatically choose the cheapest or most successful route for each transaction, reducing processing costs and chargebacks.

- Reconciliation, settlements, and reporting all live in one dashboard. That means fewer manual exports, fewer errors, and better financial oversight.

- With unified fraud prevention and centralized PCI controls, managing risk across multiple PSPs becomes both simpler and safer.

Step 3: Design for compliance & SCA from day one

In fintech, compliance is the foundation that determines how fast (and how far) you can scale. As Europe moves toward PSD3 and the new Payment Services Regulation (PSR), the bar for security, refunds, and customer protection is getting higher. Startups that design for compliance from the start won’t just stay out of trouble — they’ll build faster, earn trust sooner, and expand with fewer roadblocks.

PSD3/PSR: New Refund and Consumer Protection Rules

Under PSD3, payment service providers will have to process refunds for unauthorized transactions within 14 business days — a faster timeline than before — unless the customer is proven to be at fault.

That means your dispute-handling workflows, fraud detection, and customer support tools must be built to handle real-time evidence collection and case resolution.

PSR goes a step further, tightening how providers share fraud data and clarifying who’s liable when authentication is delegated to third parties. Together, these changes push fintechs to standardize compliance processes across all EU markets. Designing this infrastructure early avoids painful retrofits later and strengthens your brand as a trusted, regulation-ready operator.

SCA & 3DS2: Secure Payments Without Conversion Loss

Security shouldn’t come at the cost of conversion — and that’s exactly what Strong Customer Authentication (SCA) and 3D Secure 2 (3DS2) aim to balance.

SCA requires two independent factors for each electronic payment: something the user knows (like a password), something they have (like a device), or something they are (like a biometric).

3DS2 is the upgraded protocol that makes this process seamless. It passes rich contextual data (device, location, transaction patterns) to the issuing bank, allowing for smarter risk assessments. Low-risk payments can be approved instantly, while high-risk ones trigger extra verification.

When implemented from day one, 3DS2 keeps approval rates high and prevents friction that kills conversion. For fintechs targeting Europe, that’s non-negotiable.

Treat Compliance as Growth Enabler

Here’s the mindset shift: compliance can be a growth enabler.

Embedding KYC, AML, SCA, PCI DSS, and regulatory monitoring directly into your product architecture does more than satisfy auditors. It:

- Speeds up market entry by removing compliance bottlenecks.

- Builds partner confidence with banks and payment networks.

- Protects your reputation when new regulations roll out.

Step 4: Leverage Platform Features Without Getting Locked In

Stripe and Adyen make it easy to build and scale fast. Their developer-first APIs, global coverage, and built-in tools for billing, fraud detection, and authentication can give any fintech company a head start. But the more you rely on a single provider’s proprietary stack, the harder it becomes to move later.

As your company grows, so do your needs: pricing shifts, new markets open, and regulations evolve. To stay flexible, you have to design your system so you can take full advantage of platform features without tying your hands.

Minimizing Lock-In: Build for Portability

To protect flexibility, architect your payment layer around agnostic systems that make switching providers painless when the time comes.

1. Agnostic Tokenization

When storing customer card data for recurring payments or subscriptions, avoid using a PSP’s proprietary token vault. Instead, use a third-party tokenization service or orchestration platform that can securely store and migrate tokens between providers.

That way, if you ever change or add a PSP, customers won’t need to re-enter their card details — you can port the data seamlessly.

2. Webhook Abstraction

Every PSP structures its webhook events differently. To prevent chaos, create a unified event layer that interprets all incoming payment events (success, failure, dispute, refund) into a single, standardized format.

This keeps your internal systems PSP-agnostic. Swap a provider, and the business logic doesn’t break, only the connector changes.

Dual-Homing and Smart Routing

If you want real resilience, plan for parallel operation. Dual-homing means running two or more PSPs side by side, routing transactions dynamically based on geography, card type, reliability, or cost.

- If one PSP is down, traffic automatically shifts to the other.

- If one performs better in a region, you can prioritize it.

- If pricing changes, rerouting is a configuration tweak.

Combined with orchestration and tokenization, dual-homing turns your payments layer into a flexible, data-driven system instead of a single point of dependency.

Practical Recommendations

- Architect token storage and recurring billing via payment orchestration platforms or PCI-compliant third-parties (not just one PSP’s vault) for future flexibility.

- Abstract payment events/webhooks and build a unified interface for business logic to seamlessly support additional or alternative PSPs.

- Regularly benchmark PSPs on pricing, authorization rates, and feature rollout, and be prepared to reallocate volume as market or business requirements shift.

- Use the powerful fraud, billing, and compliance modules of Stripe or Adyen, but ensure systems are modular; avoid embedding proprietary logic that’s tough to replicate or port.

Wrapping Up

Stripe and Adyen give you the tools to move fast; your job is to make sure you can still move freely. Because markets shift, fees change, and regulations never stop evolving, and your infrastructure should adapt just as quickly.

Not sure if “just Stripe” is costing you approvals or fees?

At INSART, we can take a deep look under the hood.

Our team will audit your payments stack, model multi-PSP uplift, and map the local methods that matter most in your target markets. We’ll also flag any PSD3/SCA compliance gaps that could affect your conversion or risk profile — then deliver a 2-page action plan with estimated approval-rate gains and potential fee savings.

Get a benchmark of where you stand, and what your next 10% improvement could look like.