This playbook is designed as a sharp, practical guide to getting your first round right. It strips away generic advice and focuses on what actually moves the needle: defining why you’re raising, structuring the process, building a credible narrative, and executing with discipline. Every section reflects how real fundraising unfolds, from early prep to closing, highlighting where founders typically lose leverage and how to avoid it.

Read on to equip yourself with the practical tools, patterns, and actions steps you need to nail your first fundraising round.

Before You Fundraise: Get Your House in Order

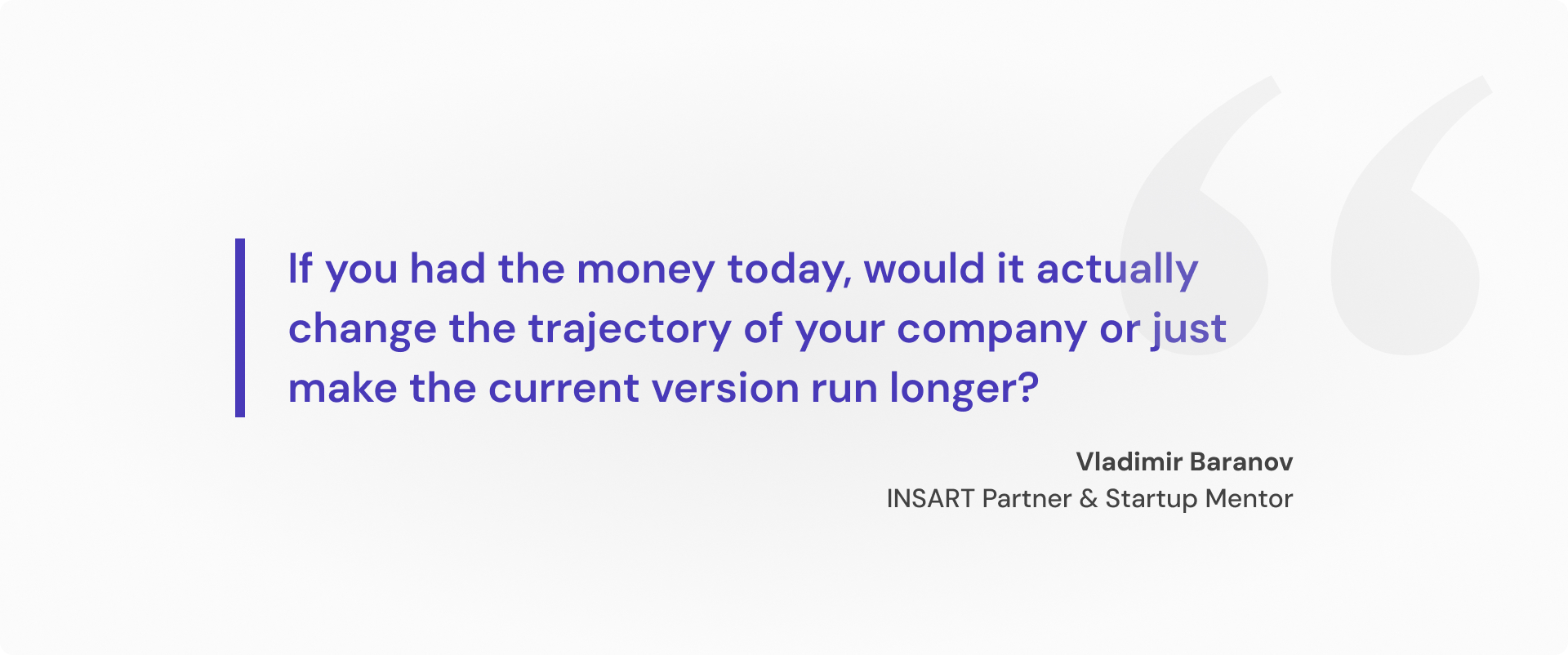

Some founders start fundraising when they feel ready emotionally but miss on the strategic part. That gap costs them months, valuation, and leverage. Before anything else, INSART Partner and Startup Mentor Vladimir Baranov has one diagnostic question he asks every founder who’s considering a raise:

It’s the single sharpest test of fundraising readiness. If your honest answer is “it would mostly extend runway,” you’re probably only ready to keep building. Capital should unlock a step-change: a new market, a product bet you can’t make scrappily, a hire that changes your ceiling. If it’s just buying time, investors will sense that before you do. If the answer leans toward trajectory change, here are a few more things to consider before you go active.

Know exactly why you’re raising

Anchor your raise to concrete milestones: ship v2 of the product, acquire 50 paying customers, or open two new markets by Q3. Each of those is something an investor can evaluate. “More runway” is not.

Write out the three things this capital will let you prove. If you can’t do that cleanly, you’re not ready to raise.

INSART tip: If your milestone list has more than three items, you’re spreading the money too thin or you haven’t prioritized. Pick the one bet that changes your trajectory most. Investors want to fund conviction, not optionality.

Size the round from the bottom up

Build a 18–24 month budget line by line including headcount, infrastructure, marketing spend, legal, buffer. Run at least two scenarios: lean (minimum to hit milestones) and full (everything you’d want). The difference between those numbers is your negotiating range. Then decide how much of the company you’re willing to sell. Seed rounds typically see 15–25% dilution. Know your number before someone else sets it for you.

Common pitfall: Founders often anchor round size to what feels impressive rather than what the math supports. Raising $2M when your model needs $800K leads to either wasted capital, overextension, or an awkward explanation at your next round.

Pick the right investor type, then build your list

Not all investor money is the same. The wrong investor type creates friction for years. Match the vehicle to your stage:

- Angels — fast decisions, small checks, useful if they’re domain experts in your space

- Pre-seed/seed funds — more process, but structured support; check their portfolio for stage fit and competitive conflicts

- Accelerators (YC, Techstars, etc.) — dilutive but network-dense; right for founders who need market validation and warm intros fast.

- Strategic investors — can open doors but can also complicate future rounds; approach with eyes open

- Family offices — often flexible terms, slower diligence; good for niche B2B plays

Once you know the type, build a tiered spreadsheet with three tiers: Tier 1 (dream list), Tier 2 (solid fit), Tier 3 (fallbacks). For each, track stage fit, sector focus, any competitive conflicts, and your warm intro path. Cold outreach works maybe 5% of the time. Build your intro paths before you need them.

INSART tip: Check every investor’s portfolio for direct competitors before you pitch. One awkward “we already backed someone in this space” kills momentum and wastes everyone’s time. Five minutes of research prevents it.

Clean your house before anyone looks inside

Investors do diligence. What they find or can’t find shapes how they see you as an operator. Before your first pitch, make sure:

- Your company is properly incorporated (Delaware C-Corp if you’re US-targeting; get this right early).

- Co-founder equity splits, vesting schedules, and any side agreements are documented and clean.

- All IP is assigned to the company (not to a founder personally, not to a former employer).

- Contractor and employee agreements are signed and current.

- Cap table is accurate and up to date.

A messy legal situation kills them slowly, after you’ve already gotten excited. Deal lawyers have seen it all; assume they’ll find whatever you haven’t fixed. Considering the following exercise to get ahead:

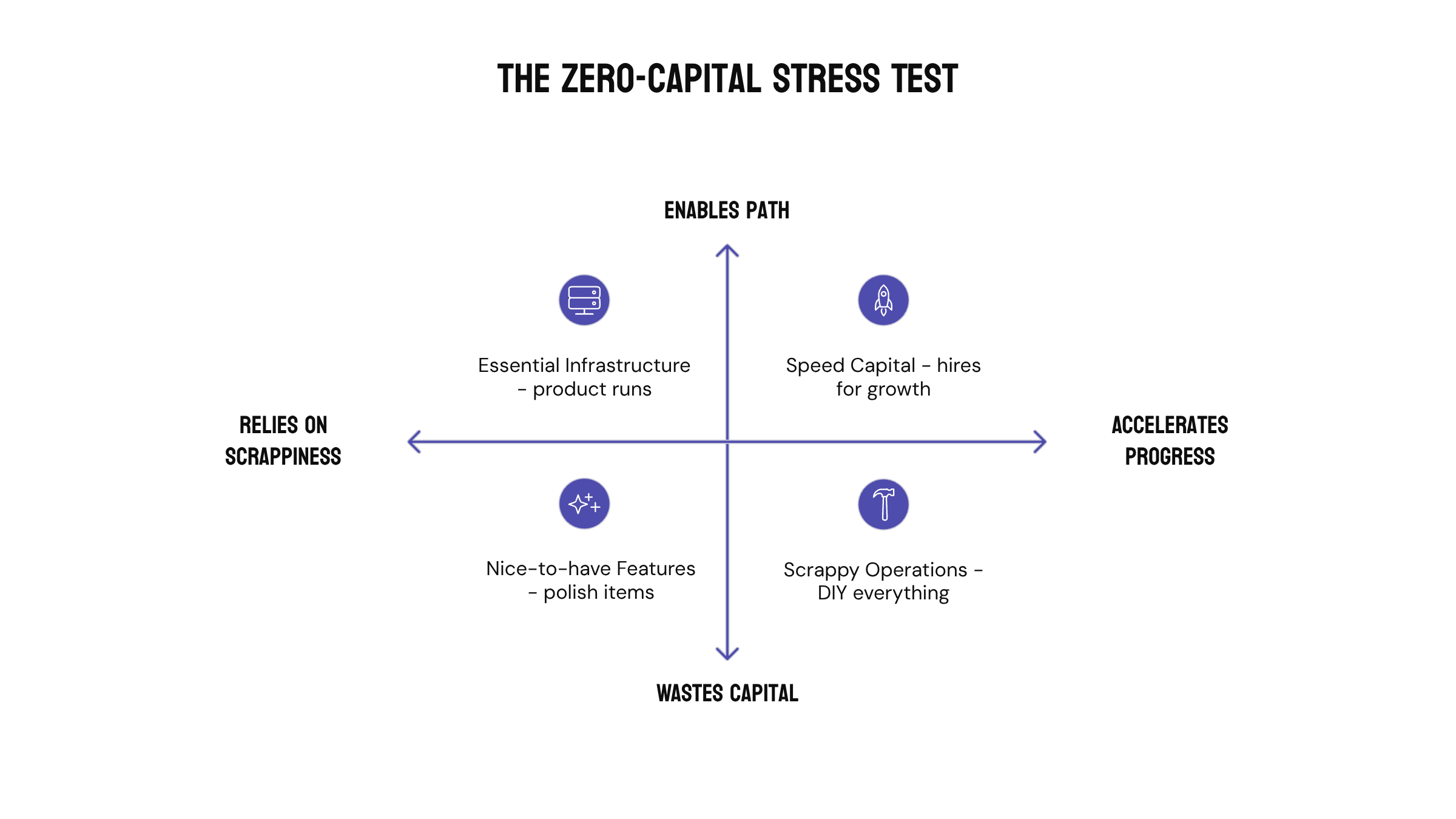

Run a zero-capital stress test

Before you commit to raising, force this question: “If we raised zero this year, how far could we actually get?”

Write out what you’d do differently. What gets cut? What gets scrappier? What still gets built? The answer reveals what capital actually unlocks versus what it just accelerates. If scrappiness gets you 80% of the way there, your raise needs a sharper story. If it genuinely blocks the path, you now have your core fundraising argument.

This exercise also sharpens your negotiation. Founders who don’t need to raise but are choosing to in order to move faster negotiate from a different position than founders who are desperate.

Core documents & data room: look ready before you feel ready

Investors form impressions fast. A disorganized or incomplete document set signals sloppy operations, so take your time to prepare everything and don’t try to build everything at once. There’s a clear sequencing here: a lean set of documents gets you through first meetings, and a full data room only needs to exist once you’ve earned genuine interest. Doing it the other way round wastes weeks on documents no one will read.

INSART tip: The moment an investor says “can you send us a data room?” is a buying signal. Have the lite version ready to share within 24 hours. Delays at that stage cost you momentum and make you look like you’re scrambling.

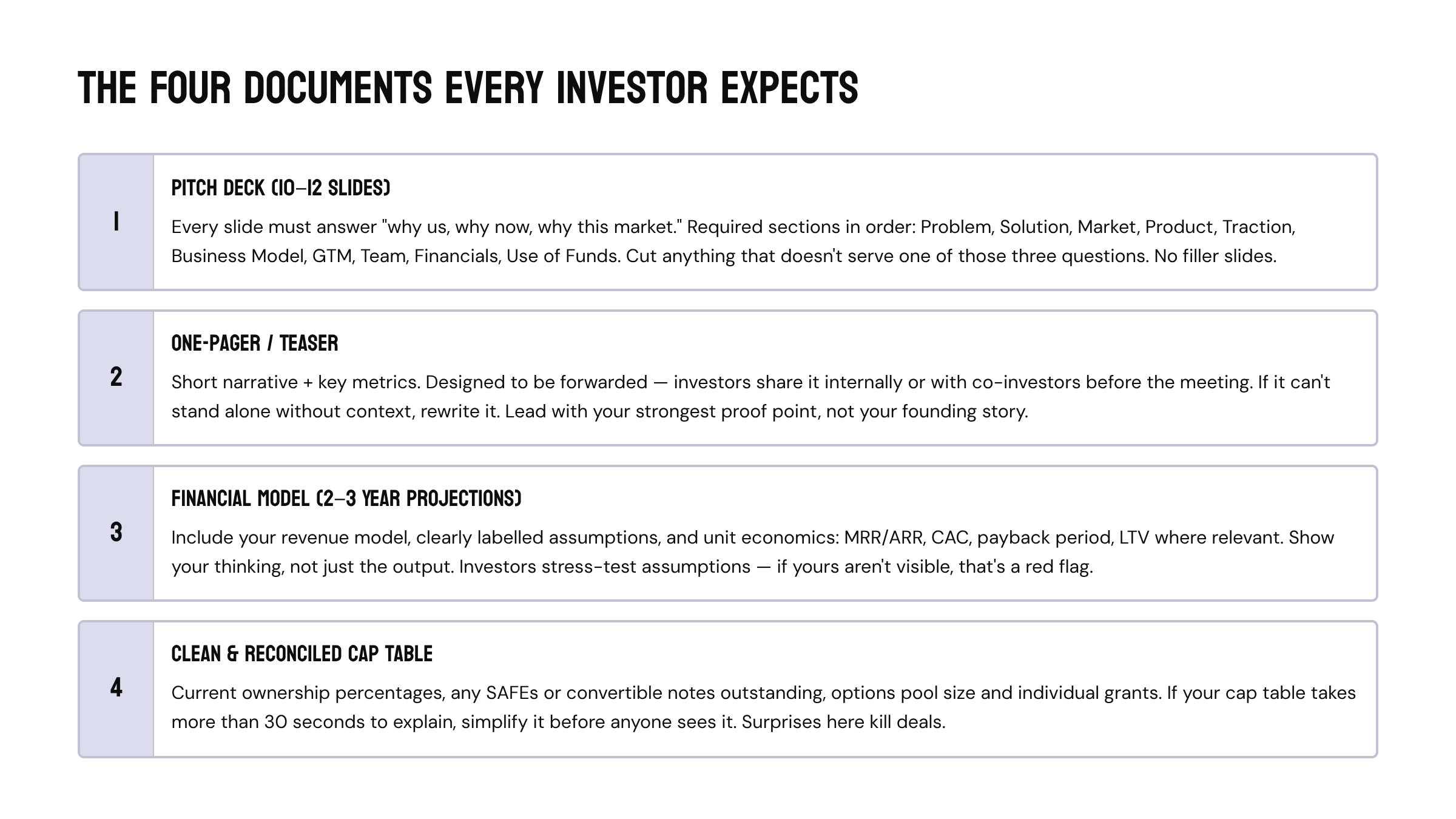

These four documents need to exist before you take a single meeting. If any are missing or rough, fix them first.

Pitch deck

Most first-time founders either over-design (beautiful slides, weak logic) or under-design (scraggly Google Slides, strong logic buried). Neither works. The deck is a narrative document, so every slide should answer one question and make the reader want to ask another. The slides investors scrutinize hardest are traction, market size, and team. Don’t bury your best numbers. Lead with them.

Common pitfall: Founders often project TAM at $500B when their real wedge addresses $30M. Investors know the difference. Use a bottom-up market size argument, including how many buyers exist, what’s a realistic price, what’s achievable in 3–5 years. Credibility over scale.

Financial model

You don’t need a perfect model. You need a model that shows you understand your business mechanics. Investors expect the numbers to change, but they’re testing whether you can reason from first principles about revenue, cost, and growth. Clearly label every assumption and never hide the inputs. If you’re pre-revenue, show unit economics from pilots, cohort data, or comparable benchmarks. “We don’t have data yet” is less credible than “here’s what we modeled and why.”

Data room lite

Once an investor moves past first meetings, they’ll want to dig deeper. This is when you open the data room. Structure it by category and don’t dump everything in one folder. Divide by corporate, legal & IP, commercial, product and metrics, and HR. Use a proper data room tool (Notion, Docsend, or Google Drive) with folder permissions. Never email zipped folders. Track who views what and for how long; it tells you who’s actually interested versus kicking tires. Docsend’s analytics have saved more than a few founders from chasing cold leads.

Crafting a strong pitch

Most founders write a deck and call it a pitch. That’s one format for one context. A real pitch is a modular story you can compress to 30 seconds or expand to 30 minutes without losing coherence. Here’s how to build it once and deploy it everywhere.

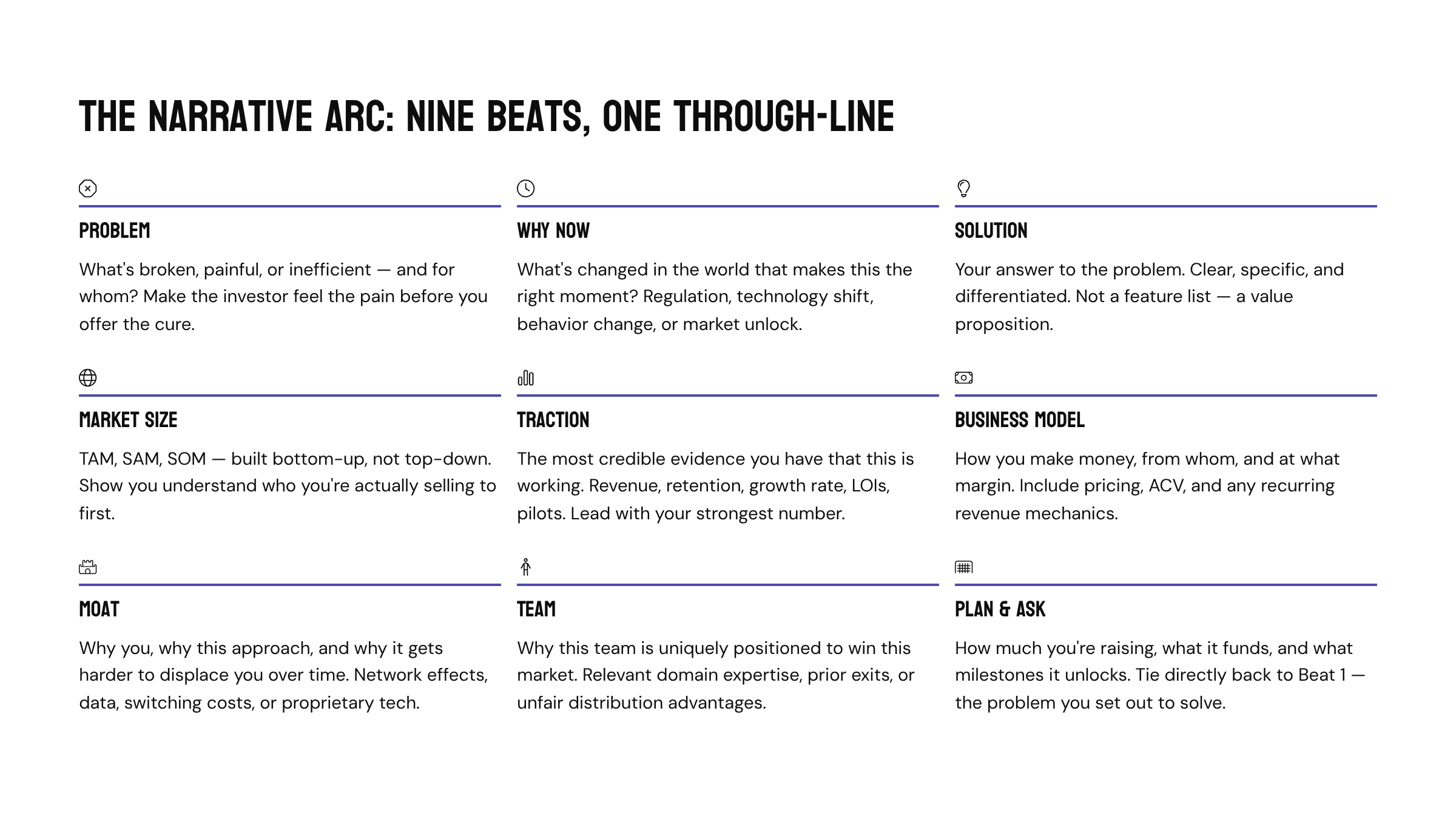

The narrative arc: nine beats, one through-line

Every strong pitch follows the same skeleton. The order matters, as it mirrors how investors build conviction. Skip or scramble beats and you lose them.

INSART tip: Write a one-sentence version of each beat before you build any slides. If you can’t distill beat 4 (market) into one crisp sentence, your thinking isn’t sharp enough yet. The sentence becomes your slide headline. The slide proves it.

Four formats, one story

You need four pitch lengths ready, with each having a different goal.

- 5 sentences cold email. The goal here is to get a reply. One sentence each: what you do, who for, traction proof point, why you’re reaching out to them specifically, the ask (15-min call). No attachments.

- 30-second elevator. The goal is to make them curious. Problem + solution + one traction stat + why now. Practice until it sounds like a sentence and end with a question.

- 3-minute teaser. The goal is to earn the 30-min meeting. Hit all nine beats in compressed form. Lead with your strongest proof point, not the problem. Assume a smart audience with no domain knowledge.

- The full 30-minutes meeting. The goal is to build enough conviction for the next step. 10 min pitch, 20 min Q&A. Don’t try to cover everything, as it’s better to leave room for dialogue. Investors who ask questions are engaged; let them.

Common pitfall: Founders treat the deck as the pitch. It isn’t. The deck is a leave-behind teaser to get the meeting. If you’re reading your slides, you’ve already lost the room. Know the story cold and use slides as anchors.

Every claim in your pitch needs a proof point or it costs you credibility, so replace adjectives with data.

- “Rapid growth” → MRR grew 22% MoM for the last 4 months

- “Strong retention” → 92% 6-month retention, net revenue retention of 118%

- “Customers love it” → NPS of 67; three enterprise pilots converted to paid contracts

- “Huge market” → bottom-up: 40,000 target buyers × $18K ACV = $720M addressable

Pre-revenue? Use proxies: LOIs, pilot agreements, waitlist conversion rates, benchmark comparisons from comparable companies at your stage. “We don’t have revenue yet” is survivable. “We don’t have evidence anyone wants this” is not.

Practice as the only way to get good

One practice pitch is not enough. Ten is a start. You need enough reps that the story feels inevitable and that you’ve heard every hard question at least twice before a real meeting. Run pitches in this order: friendly advisors first (for structure feedback), then early-stage founders (for investor simulation), then angels you’re less excited about (real reps with low stakes), then your target list. Use every meeting to collect the questions you didn’t have a great answer to. That’s your prep list for the next one.

INSART tip: After every pitch, write down every question you stumbled on and then come up with a crisp two-sentence response. Read it before your next meeting. The questions that keep coming up are telling you something is unclear in the pitch itself, not just that you need a better answer.

Running the process: fundraising is a sprint, not a drip

Fundraising done passively takes 9 months and kills your momentum. Done intentionally, it takes 6–10 weeks. The difference is treating it like a sales process with a defined timeline, a managed funnel, and deliberate communication. Here’s the playbook.

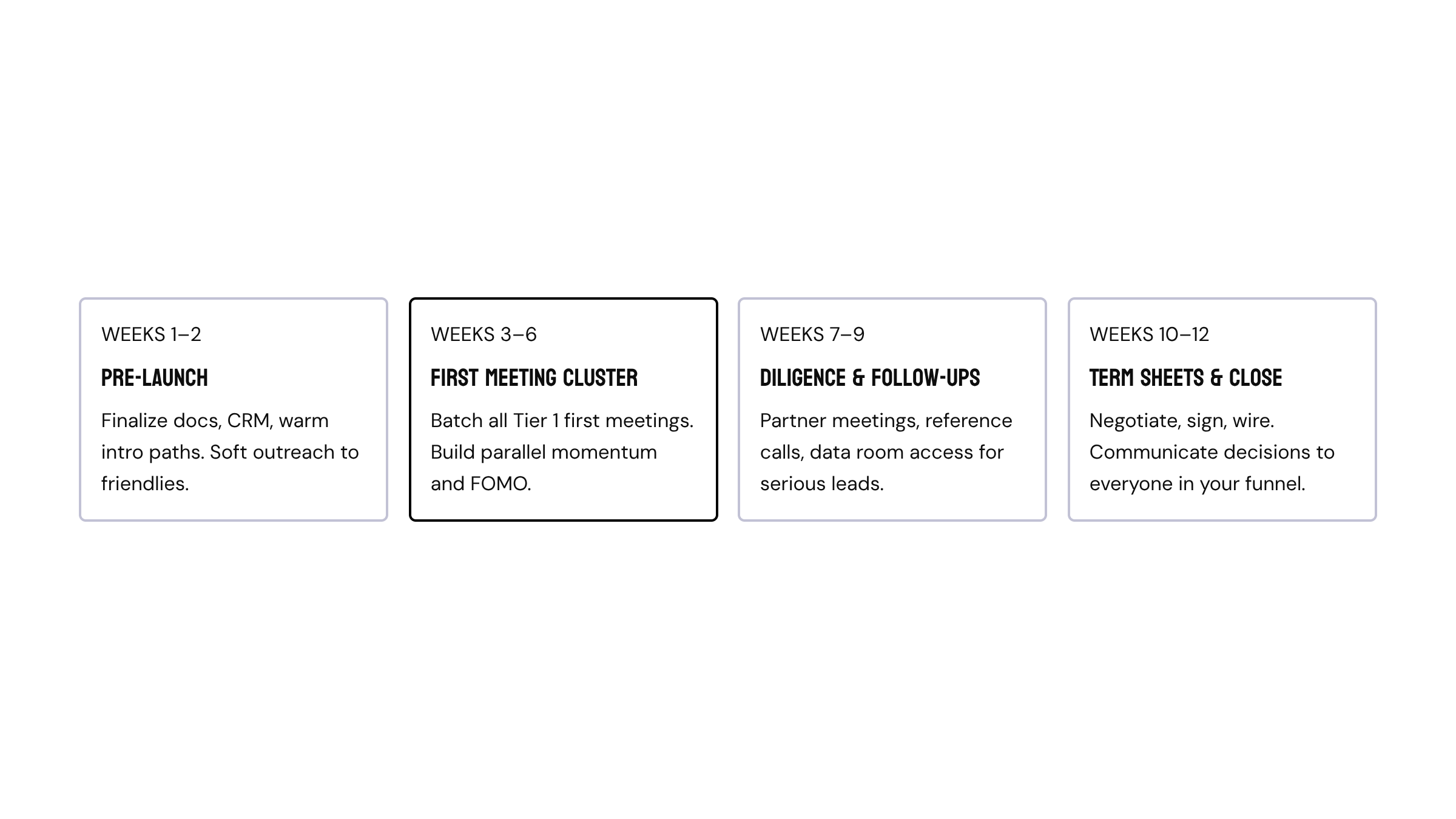

Time-box the raise from day one

Set three dates before you start: when you go active, when first meetings should be clustered, and when you expect to close. Without these, the raise expands to fill all available time, which means months of distraction with no result. A realistic seed raise timeline looks like this:

The most important window is weeks 3–6. That’s when you want maximum simultaneous activity. If meetings are scattered across three months, you lose the pressure that drives decisions.

Warm intros first: cold outreach is a last resort

A warm intro converts at roughly 10–20x the rate of a cold email. Before you send anything cold, exhaust every intro path: portfolio founders at funds you’re targeting, operators in your space, angels who know your Tier 1 funds, accelerator networks, co-investors from prior rounds. For each target investor on your list, you need an answer to: “Who do I know that this person would take a call from?” If the answer is no one, work on the relationship first or move them to Tier 2.

Batch meetings to manufacture momentum

The single biggest process mistake founders make is spreading meetings across weeks because “we’re not ready yet” or “let’s take it slow.” This destroys your leverage. Compress your Tier 1 first meetings into a 2–3 week window. Delay any investor who wants to move fast by a week or two rather than let them run ahead of the pack. The goal is decisions converging at roughly the same time.

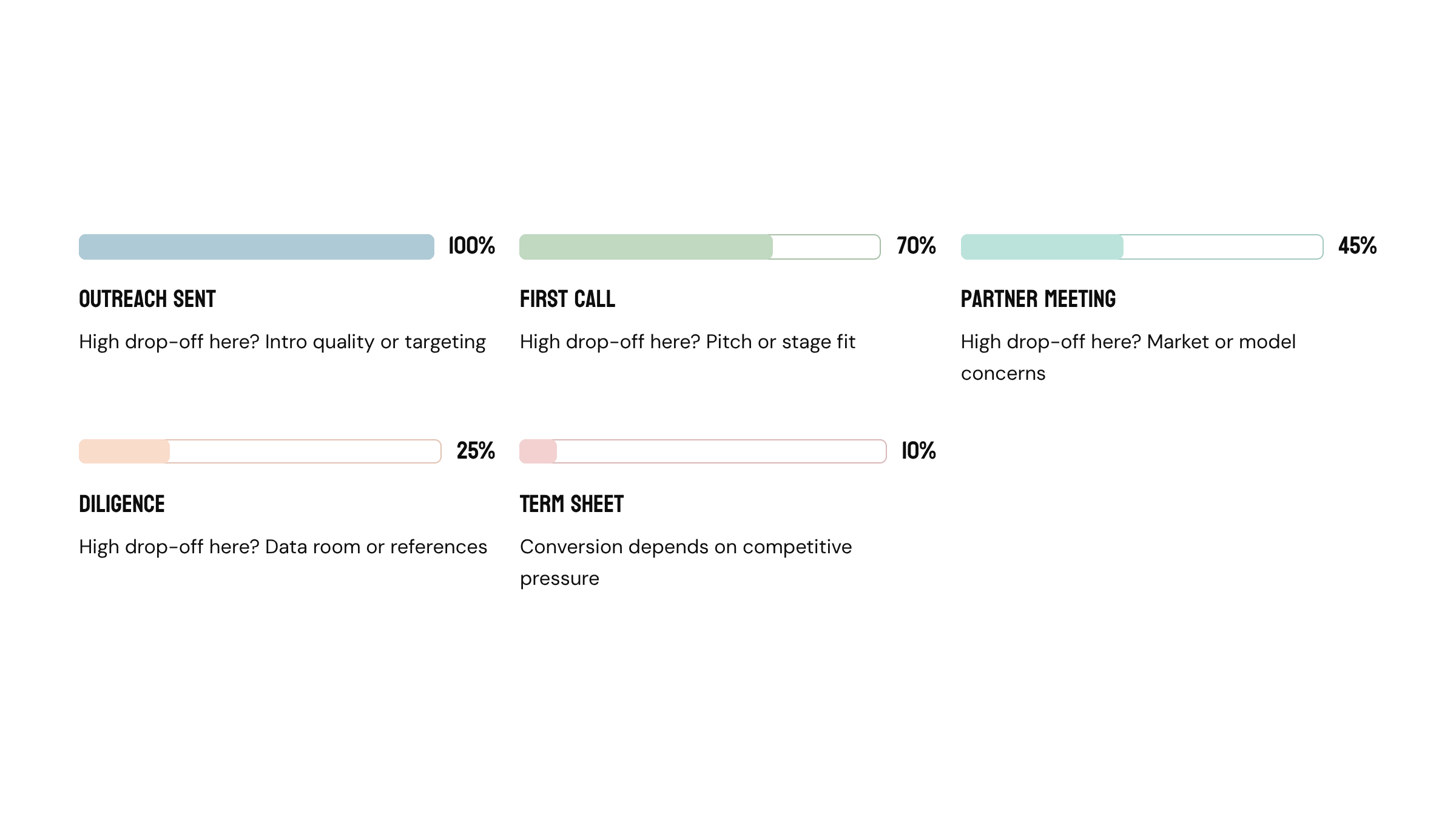

Track your funnel like a sales pipeline

If you’re not tracking every investor in a CRM or spreadsheet with stage and last-touch date, you will drop follow-ups, lose momentum, and have no idea where your process is breaking down. Your fundraising funnel has five stages. Know your conversion at each one, and when drop-off is high, diagnose whether it’s a pitch problem, a fit problem, or a timing problem.

Communicate momentum throughout the raise

Investors who heard your pitch three weeks ago and haven’t heard from you since have moved on mentally. Your job is to stay top of mind with real signal. Every 2–3 weeks, send a short investor update to everyone in your active funnel: warm leads, first-meeting done, diligence in progress. Include one or two real developments: a customer win, a product milestone, a hire, a metric move. Keep it under 200 words and make it easy to forward.

Term sheets, diligence & closing: get to money-in-bank, not just signed

A term sheet is not a closed round. Founders celebrate too early, slow down, and then watch deals die in diligence or legal. The last 20% of the process requires the same intensity as the first 80%. Here’s how to finish clean.

Comparing offers: valuation is not the only number

When you have multiple term sheets, founders almost always anchor on the highest valuation. That’s often the wrong call. A higher number from the wrong partner, with worse terms and no follow-on capacity, will cost you more at Series A than the dilution you saved at seed.

Evaluate offers across at least five dimensions:

| What to compare | Why it matters | Weight |

| Partner quality | Who specifically will be on your board/in your corner? Have they helped founders navigate hard moments, or just the easy ones? Call 3–4 portfolio founders, including ones who had a tough year. | High |

| Valuation & dilution | Pre-money and post-money, including pool refresh. Important, but not the only number: a 15% valuation premium doesn’t matter if the partner is a nightmare or the fund is too small to follow on. | Medium |

| Check size & follow-on | Does this fund have the capacity to lead or participate in your Series A? A $50M seed fund with a $500K check probably can’t. That matters when you need a signal investor at the next round. | High |

| Terms beyond valuation | Liquidation preference, board seats, pro-rata, protective provisions. One aggressive term can more than offset a higher headline number. Model the downside scenarios, not just the upside. | High |

| Network & value-add | Be honest here: most seed investors are not as hands-on as their pitch implies. Ask specifically: “Who have you introduced to customers in my space in the last 12 months?” Specificity reveals reality. | Medium |

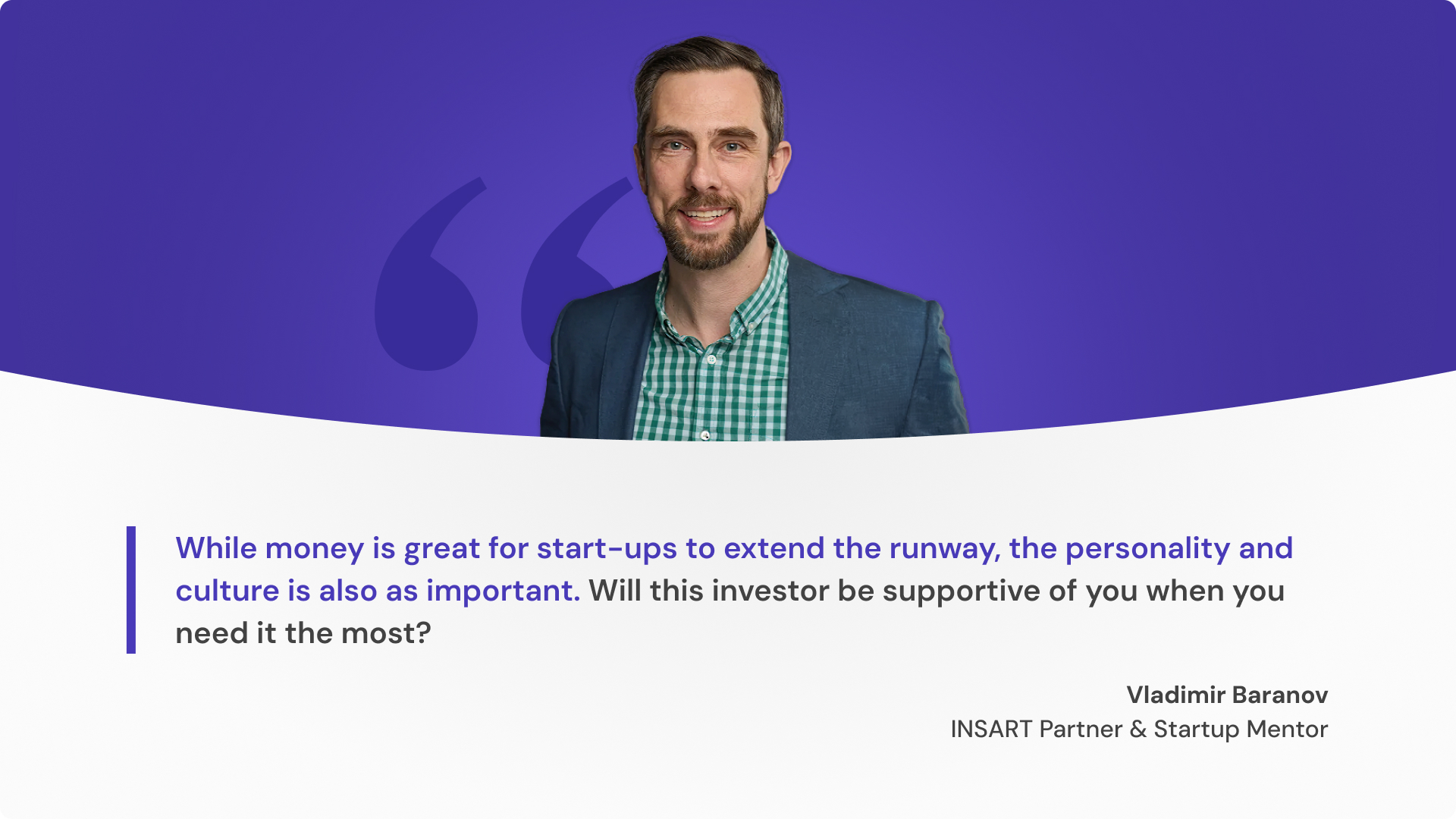

Lastly, choosing an investor is far more than a financial decision. It’s a relationship you’ll be in for years, through good quarters and bad ones. Vladimir Baranov makes a point of reminding founders that the money is only part of the equation:

Legal diligence: fix it before they find it

Diligence is not a formality. Investors are specifically looking for anything that could blow up the deal or become a liability post-close. The best approach is to audit your own data room before you send it to find the gaps yourself and fix them proactively. The items that kill or delay deals most often:

- Cap table discrepancies — SAFEs or notes that weren’t tracked, options that were granted but never documented, wrong share classes. Run a full reconciliation before diligence opens.

- Missing IP assignments — A contractor built a core feature two years ago and never signed an assignment. That’s an existential issue. Chase it down before anyone asks.

- Undisclosed material contracts — exclusivity clauses, revenue share arrangements, customer contracts with change-of-control provisions. Investors need to see these; surprises during diligence are deal-killers.

- Corporate approval gaps — board consents missing for prior equity issuances, founder agreements that predate incorporation. Your lawyer can remediate most of these; just do it early.

INSART tip: Run a mock diligence on yourself before you open the data room. Pretend you’re the investor’s lawyer and look for anything that would make you pause. Whatever you find, fix it or prepare a clear explanation.

Post-close: stop fundraising, start building

The day after close, founders often feel a kind of blank exhaustion. That’s normal. What’s not normal, but very common, is staying in fundraising mode for weeks after: taking “relationship” calls, tweaking the deck, keeping options open. You raised, now it’s time to execute.

- Set update cadence. Monthly for lead investors, quarterly for angels. Make them short, consistent, and honest.

- Agree on metrics. Align with your board on 3–5 key metrics that define success for this stage. Ambiguity about what “good” looks like leads to painful board meetings later.

- Refocus on product. The milestones you pitched to raise this round are now your job. Block fundraising-mode habits: fewer investor calls, more customer calls. Build the thing.

One last thing: tell every investor who went through the process with you, even those who passed, that you’ve closed. It’s professional, it keeps the relationship warm for the next round, and it closes the loop on a process they invested time in. Most founders don’t do this, so be the one who does.

A closed round is a starting line, not a finish line. The founders who make the most of it are the ones who got back to building the fastest. You know what to do. Go do it.

")

![[SIGNALS] Banner & visuals for the Interview_ Giorgio Natili (1)](https://insart.com/wp-content/uploads/2026/05/signals-banner-visuals-for-the-interview_-giorgio-natili-1-300x169.jpg "The Best Scaling Decision You'll Make Has Nothing to Do With Infrastructure: Conversation with Giorgio Natili")